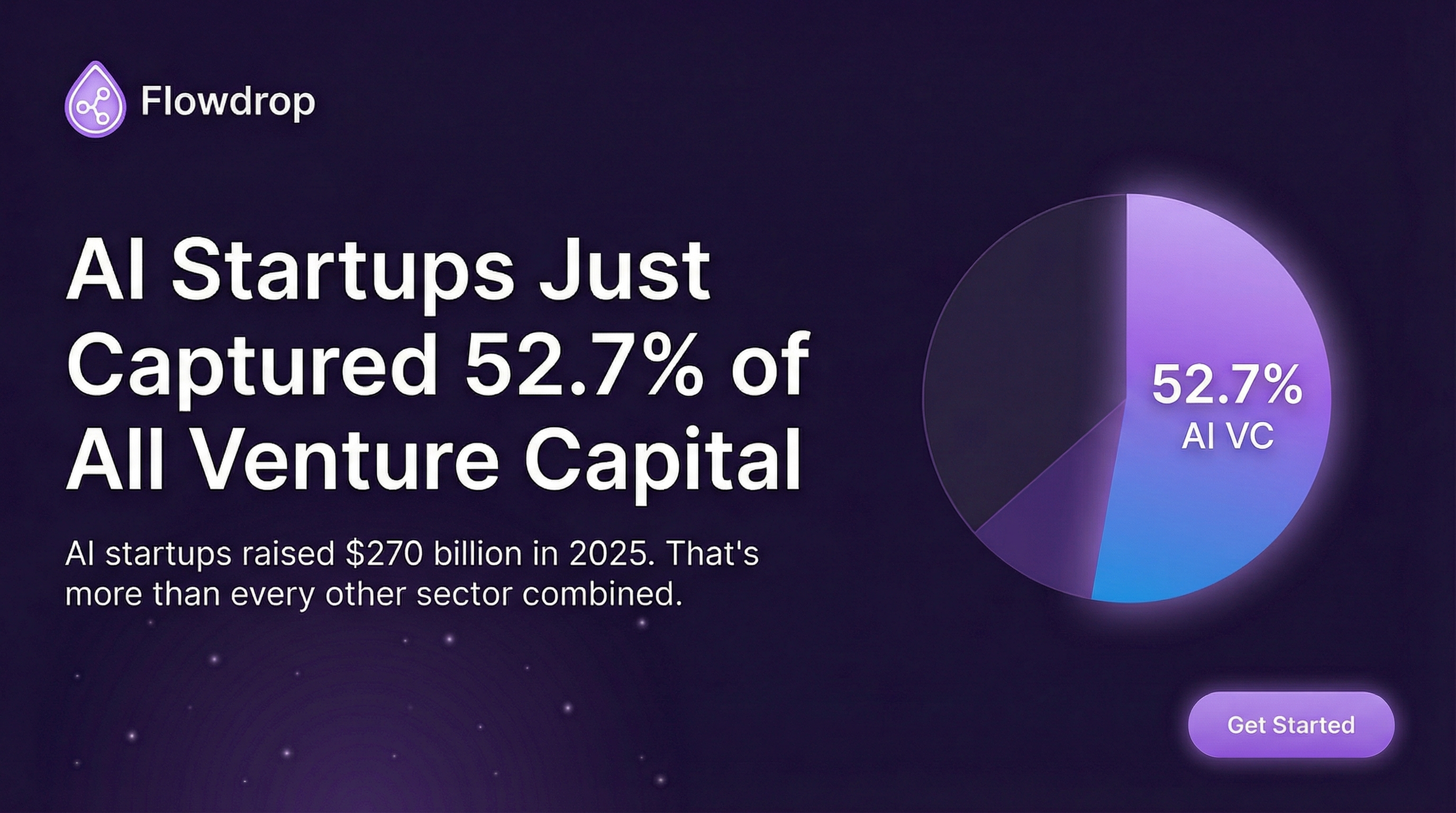

AI Startups Just Captured 52.7% of All Venture Capital

AI startups raised $270 billion in 2025—more than every other sector combined. For the first time in VC history, artificial intelligence absorbed over half of all global funding. Here's what it means.

AI startups raised $270 billion in 2025.

That's more than every other sector combined.

For the first time in venture capital history, artificial intelligence companies absorbed 52.7% of all VC funding worldwide. This isn't a trend anymore—it's a complete restructuring of how capital flows through the innovation economy.

In 2023, AI companies raised 27.5% of venture capital. By 2024, that jumped to 40%. Now we're at 52.7%. That's $270 billion out of $512.6 billion invested globally last year.

North American AI startups dominated with $214.5 billion, nearly 80% of global AI investment. European companies attracted $36.7 billion. Asian startups raised $15.3 billion. Everyone else combined for $3.9 billion.

What changed wasn't the number of deals—overall deal counts actually continued declining from 2022 highs. What changed was the size of individual rounds. Investors are writing bigger checks to fewer companies.

SoftBank invested $40 billion in OpenAI. That's the largest private-company funding round in history. Not the largest tech round. The largest private-company round, period.

Meta put $14.3 billion into Scale AI. Anthropic raised $13 billion at a $183 billion valuation. These aren't seed rounds or Series A financings. These are nation-state level capital deployments going into companies that didn't exist five years ago.

AI investment stayed elevated throughout 2025, ranging from $56.9 billion to $75.5 billion every quarter. Meanwhile, non-AI sectors raised between $56 billion and $66 billion per quarter—less than AI alone.

AI startup exit value hit $189.6 billion in 2025, accounting for 34.5% of all global VC exits. That's up from 21.8% in 2024.

This matters because it means liquidity is returning. Late-stage AI companies aren't just raising capital—they're actually finding buyers or going public. The market isn't just speculating on AI's future value; it's realizing actual returns.

Previous tech booms were driven by consumer adoption curves. The internet boom was about getting people online. The mobile boom was about smartphones reaching everyone. The cloud boom was about companies moving infrastructure.

This AI boom is different. It's not waiting for adoption—it's creating infrastructure that every other company will need. AI isn't a product category that you choose to buy or skip. It's becoming the foundation layer for how software works.

That's why investors are concentrating capital into a small group of companies with proven technology. The winners in AI infrastructure will capture value from every downstream application. It's like investing in electricity generation when power grids were being built.

Here's what's weird: AI deal counts are stable, but overall venture deal volume is declining. AI accounted for 31.4% of all VC deals in 2025, up from 20.5% in 2021.

This means investors are actively choosing AI over other sectors. Dollars that would have funded SaaS companies, consumer apps, or hardware startups are flowing into AI instead.

It's not that AI is growing while other sectors stay flat. AI is growing while other sectors are shrinking. Capital is being reallocated, not expanded.

If you're raising money for a non-AI startup right now, you're competing for less than half the capital that was available a few years ago. The pool of available VC dollars for traditional tech companies has effectively been cut in half.

Average deal sizes in non-AI sectors are shrinking. Rounds are taking longer to close. Valuations are compressing. Meanwhile, AI companies are raising at multiples that would have seemed absurd in 2022.

This creates a two-tier venture market: AI companies with near-infinite capital access, and everyone else fighting for scraps. It's not fair, but it's reality.

Alan Goldberg from BestBrokers nailed it: "This shift was not driven by a surge in deal volume, which continued to decline across the market, but by a sustained increase in average deal size as investors concentrated capital into a smaller group of companies with proven technology, infrastructure relevance, and credible paths to scale."

Infrastructure relevance is the key phrase. Investors aren't funding AI chatbots or AI assistants or AI productivity tools. They're funding the companies that will provide compute, training, inference, and model infrastructure to everyone else.

That's why OpenAI, Anthropic, and Scale AI can raise billions while hundreds of AI application companies struggle to raise Series A rounds. The big money is betting on picks and shovels, not gold miners.

Goldberg also noted that the AI investment cycle is entering a more mature phase "characterized by capital-intensive competition among a handful of global players."

This is code for: the window for new AI infrastructure companies is closing. The market has picked its horses. Now those horses are racing to build moats through scale, model performance, and ecosystem lock-in.

If you're starting an AI infrastructure company in 2026, you're not competing with other startups. You're competing with multi-billion-dollar war chests and teams that have three-year head starts.

What's remarkable about 2025 wasn't just the total dollars—it's that AI absorbed roughly half or more of all VC capital in every single quarter. This wasn't a spike or a bubble burst. It was sustained, consistent preference for AI over every other category.

- Q1: 50%+ to AI

- Q2: 50%+ to AI

- Q3: 50%+ to AI

- Q4: 50%+ to AI

That's not volatility. That's a new baseline.

The data suggests we're past the experimental phase of AI investing. Investors aren't taking exploratory bets on whether AI will matter. They're making massive infrastructure bets on companies they believe will power the next 20 years of software.

This creates interesting dynamics:

Application layer opportunity: While infrastructure funding is locked up, there's still white space in vertical AI applications that solve specific industry problems.

Services and implementation: Companies that help businesses deploy and integrate AI will see growing demand as enterprise adoption accelerates.

Differentiation matters more: Generic AI products won't get funded. You need a specific wedge, unique data, or distribution advantage that infrastructure players can't replicate.

We just watched venture capital restructure itself around a single technology category in less than three years. That's unprecedented.

AI isn't a sector anymore. It's the sector. Everything else is competing for what's left.

If you're building a company in 2026, you have two choices: figure out how AI makes your product category-defining, or accept that you're competing for a shrinking pool of capital against founders who are making that choice.

The market has spoken. It's not subtle. $270 billion in one year to one category is as clear a signal as investors can send.

The question isn't whether AI is the future. The question is whether your company has a plan for existing in a world where AI companies have functionally unlimited capital and everyone else doesn't.

Data compiled from Pitchbook, CB Insights, and financial disclosures from leading venture firms via BestBrokers research.

Building in the AI era? Flowdrop helps you automate workflows without writing code—so you can focus on what makes your product unique.

Related Resources

- Ex-OpenAI Researchers Raise $150M to Fix AI's Biggest Problem — Interpretability at scale

- ElevenLabs Just Raised $500M at $11 Billion Valuation — Voice AI infrastructure

- AI Agents Replacing Manual Workflows in 2026 — Automate repetitive work

Questions? Contact us or check out our documentation.

Frequently Asked Questions

About Flowdrop Team

We build AI workflow automation tools for non-coders. Our mission is to make automation accessible to everyone, so you can focus on work that actually matters.